1031 Exchange

Understanding the potential of Section 1031 exchange and Delaware statuatory trusts

Navigating the complex tax rules of a section 1031 exchange can be a complicated experience. We simplify and streamline the process so that more investors can enjoy the benefits of Section 1031 and DST ownership.

Your team at FFC has access to properties across the nation by working with many real estate partners who sponsor quality Delaware Statuatory trust (DST) real estate investments with low investment minimums to provide investors:

- Access to real estate they would not otherwise be able to afford on their own.

- A largely automated, simplified exchange process.

- The ability to diversify their investment into multiple properties to reduce risk.

- A pipeline of qualifying replacement properties where due diligence has been completed.

________________________________________________

What is a "like-kind exchange"?

Section 1031 of the Internal Revenue Code, commonly referred to as a "like-kind exchange," allows for the complete deferral of all federal and state taxes on the sale of investment real estate.

The seller of a relinguished property must reinvest sale proceeds into a "like-kind" property, which can be any type of real estate (personal property does not qualify).

The gain that would be recognized in a taxable sale is deferred until the replacement property is sold in a taxable transaction. Taxpayers may also structure a series of exchanges, compounding the benefits of tax deferral, therby building wealth over time.

Read more about "like-kind" exchanges:

- In most deferred exchanges, taxpayers engage a "qualified intermediary" to prepare an exchange agreement and hold the net sales proceeds in an exchange escrow account pending aquisition of the replacement property.

________________________________________________

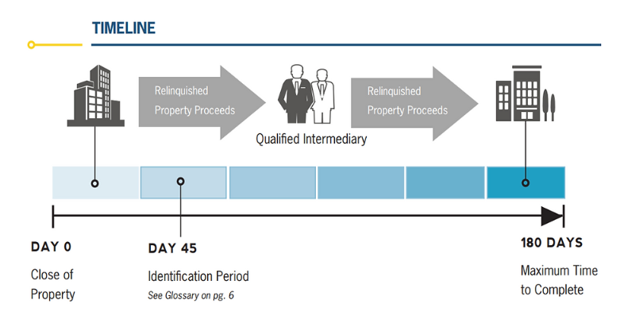

1031 Exchange Rules to Follow

For Complete Tax Deferral, Investors must:

- Use a Qualified Intermediary

- Reinvest 100% of the net proceeds and debt

- Be the same taxpayer during the exchange

- Identify potential replacement in 45 days

- Close on replacement property(s) in 180 days

________________________________________________

What is a Delaware Statutory Trust (DST)?

A Delaware Statutory Trust (DST) is a private real estate investment vehicle that allows investors to participate in a Section 1031 exchange and receive passive income as well as potential for appreciation from real estate ownership. This equation provides the potential for superior risk-adjusted returns.

The DST owns 100% of the real estate, and the investors own the beneficial interests in the DST.

Read more about DST's:

Investors have no personal liability

Investors do not provide tax returns to lenders or sign loan documents because the lender does not underwrite investors; the sponsor signs any carve-out guaranty.

Lower investment minimums mean that a greater number of investors can participate.

The simple investment process allows access to more investors.

The sponsor manages the property and makes decisions when necessary.

A DST is a distinct legal entity created as a trust under the statutory law of Delaware. In a DST, each owner is treated as owning an undivided interest in the real estate for tax purposes. FFC's real estate partner's DST offerings comply with the requirements of IRS Revenue Ruling 2004-86. Each owner's beneficial interest is treated as a direct interest in real estate for tax purposes.

________________________________________________

Contact us today for more details, properties available, and specific case studies pertaining to you or your client's situation.

Please note 1031 Exchange DSTs are restricted to Accredited Investors**

**Accredited investors are typically defined as having a $1 million net worth excluding primary residence or $200,000 income individually/$300,000 jointly of the last two years; or have an active Series 7, Series 82, or Series 65. Individuals holding a Series 66 do not fall under this definition.

IRC Section 1031, IRC Section 1033 and IRC Section 721 are complex tax concepts; therefore, you should consult your legal or tax professional regarding the specifics of your individual situation. There are material risks associated with investing in private placements, Delaware Statutory Trusts ("DSTs") and real estate securities including the potential loss of the entire investment principal, illiquidity, tenant vacancies impacting income and revenue, general and real estate market conditions, lack of operating history, interest rate risks, competition, including the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi-family properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and investors should read the PPM carefully before investing paying special attention to the risk section.